Choosing the Right Wealth Adviser After a Divorce

By Jennifer Crum, AAML — Hanson Family Law Group, San Mateo County & Timothy J. Keating — Cerity Partners

Originally published in the ACFLS Family Law Specialist, Winter 2026, No. 1

Abstract

When a marriage ends, particularly one involving significant assets, clients face a flood of financial decisions and information. Choosing a new wealth adviser is one of the many important decisions an out-spouse must make to move forward successfully. This article provides an attorney-friendly framework for answering client questions about how advisers work, how they are compensated, and how to evaluate an adviser before hiring one. We also highlight trade-offs between large brand-name institutions and independent fiduciary firms, dispel common myths, and outline key questions clients should ask to ensure they find an adviser who is the right personal and professional fit.

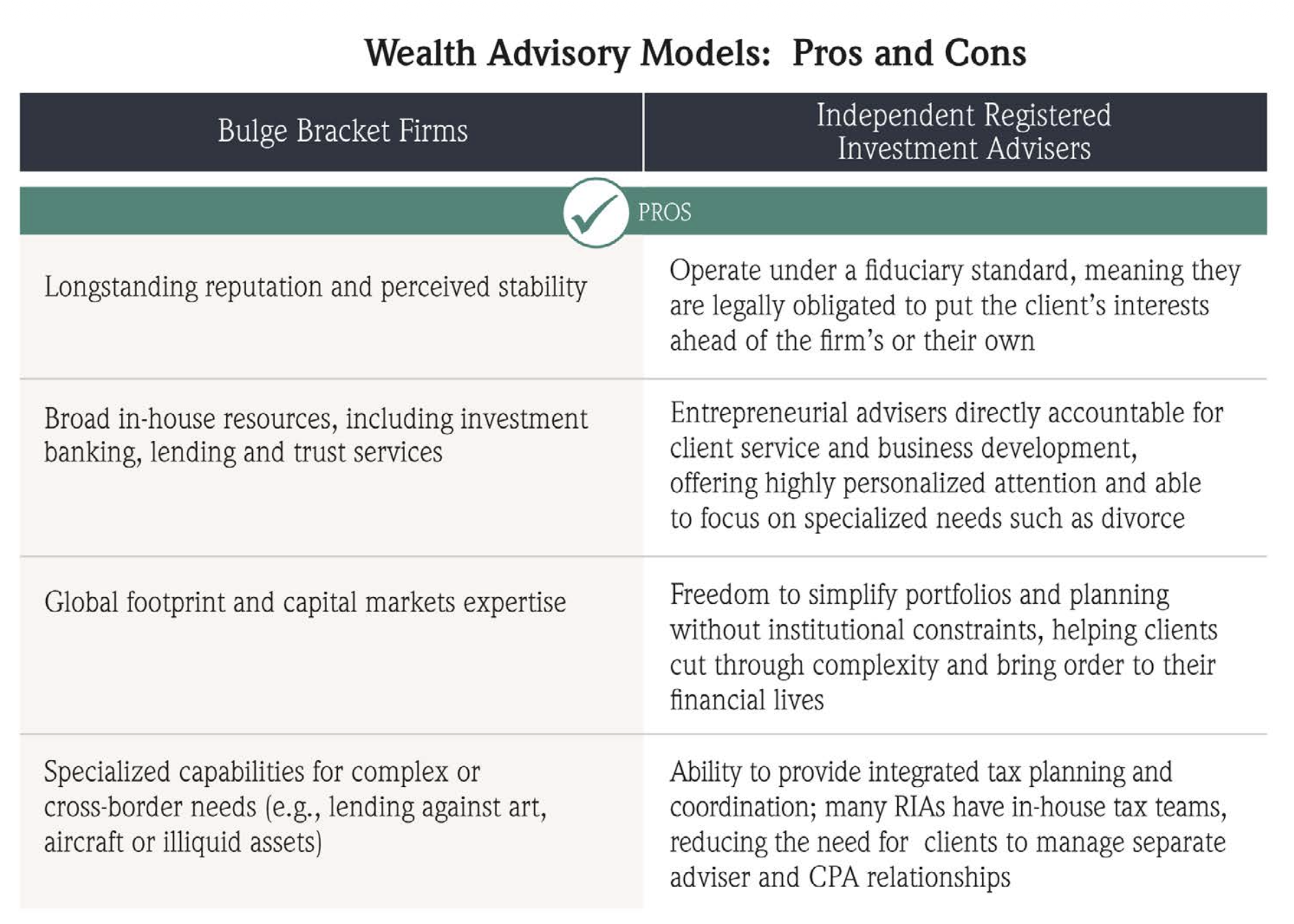

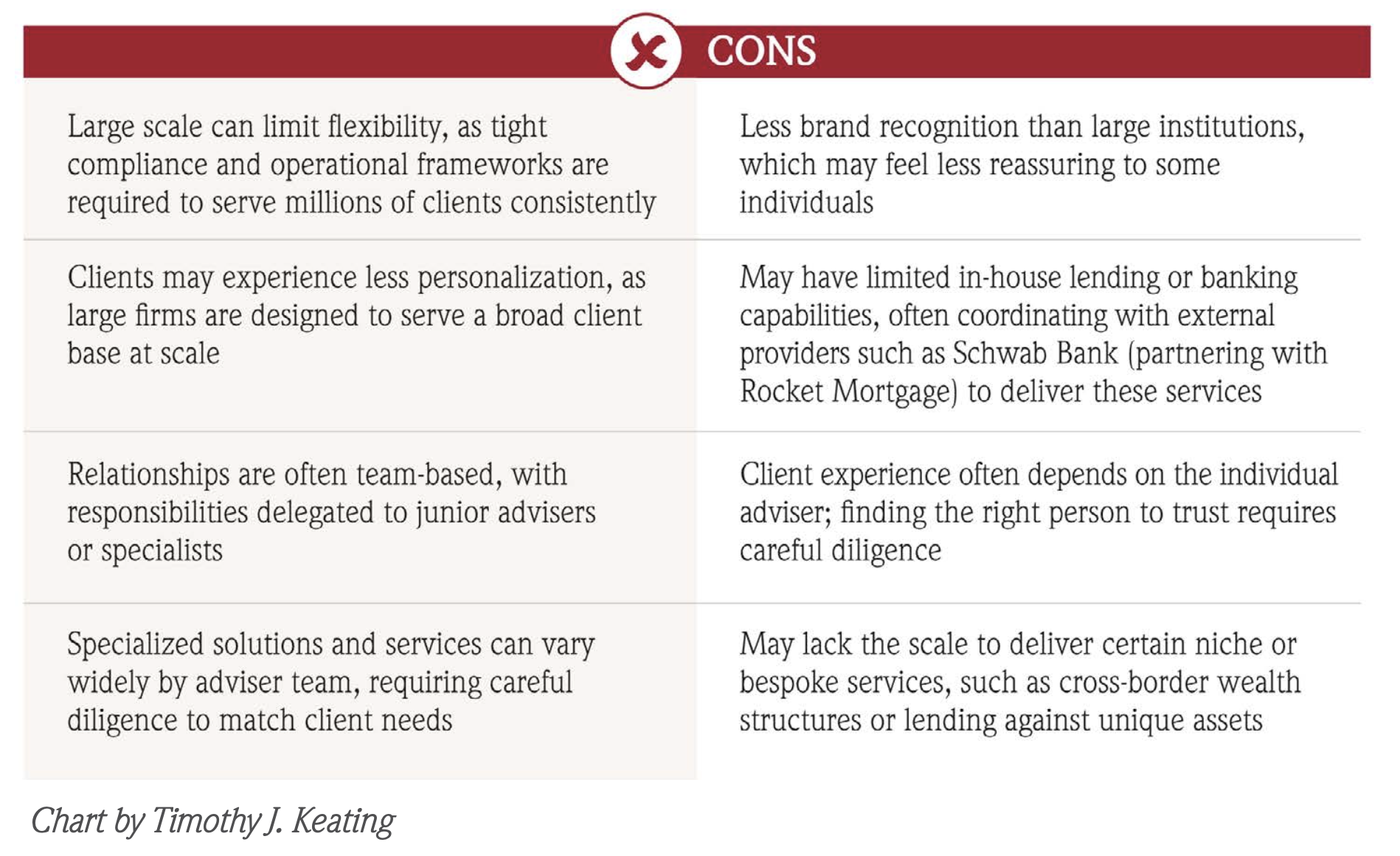

Beyond the Brand

When a marriage ends, especially one involving significant assets, the financial aftermath can be difficult to navigate without the personal and professional relationships the couple historically relied upon. Amid legal negotiations, asset divisions, and shifting family dynamics, out-spouses must make a critical decision: Who should they trust to advise them going forward?

This isn't just a practical choice—it sets the tone for their future financial life. And for many, especially those who haven't managed their finances for years, it can feel overwhelming. Choosing the right wealth adviser after a divorce is one of the most consequential decisions for moving forward successfully.

"The answer often comes down to this: You're not hiring a brand. You're hiring a person."

Three myths family lawyers commonly believe about the largest firms

Myth #1: Only the largest firms have access to the best research.

Reality: Institutional research is widely available at both large firms and RIAs. The differentiator is how effectively an adviser applies it to a client's situation.

Myth #2: They offer unique investment products that smaller firms can't access.

Reality: Today, large firms and RIAs can all access similar investment solutions. The key difference is the implementation of those solutions within a client's broader plan.

Myth #3: They offer more choice among fee models.

Reality: Most firms—including large institutions and independent RIAs—rely on a similar fee model based on assets under management, with some offering hourly or flat-fee alternatives.

A typical tiered fee structure might look like this:

100 basis points (1.00 percent) on the first $3 million

75 basis points (0.75 percent) on the next $7 million

50 basis points (0.50 percent) on assets above $10 million

For example, a $5 million portfolio would incur approximately $45,000 in annual fees (0.90 percent), while a $10 million portfolio would incur approximately $82,500 in annual fees (0.83 percent). Most firms bill quarterly in advance, deducting fees directly from the client's investment account. For clients with substantial assets—typically $25 million or more—many firms are willing to offer lower blended rates or even flat quarterly fees, reflecting the scale and complexity of the relationship.

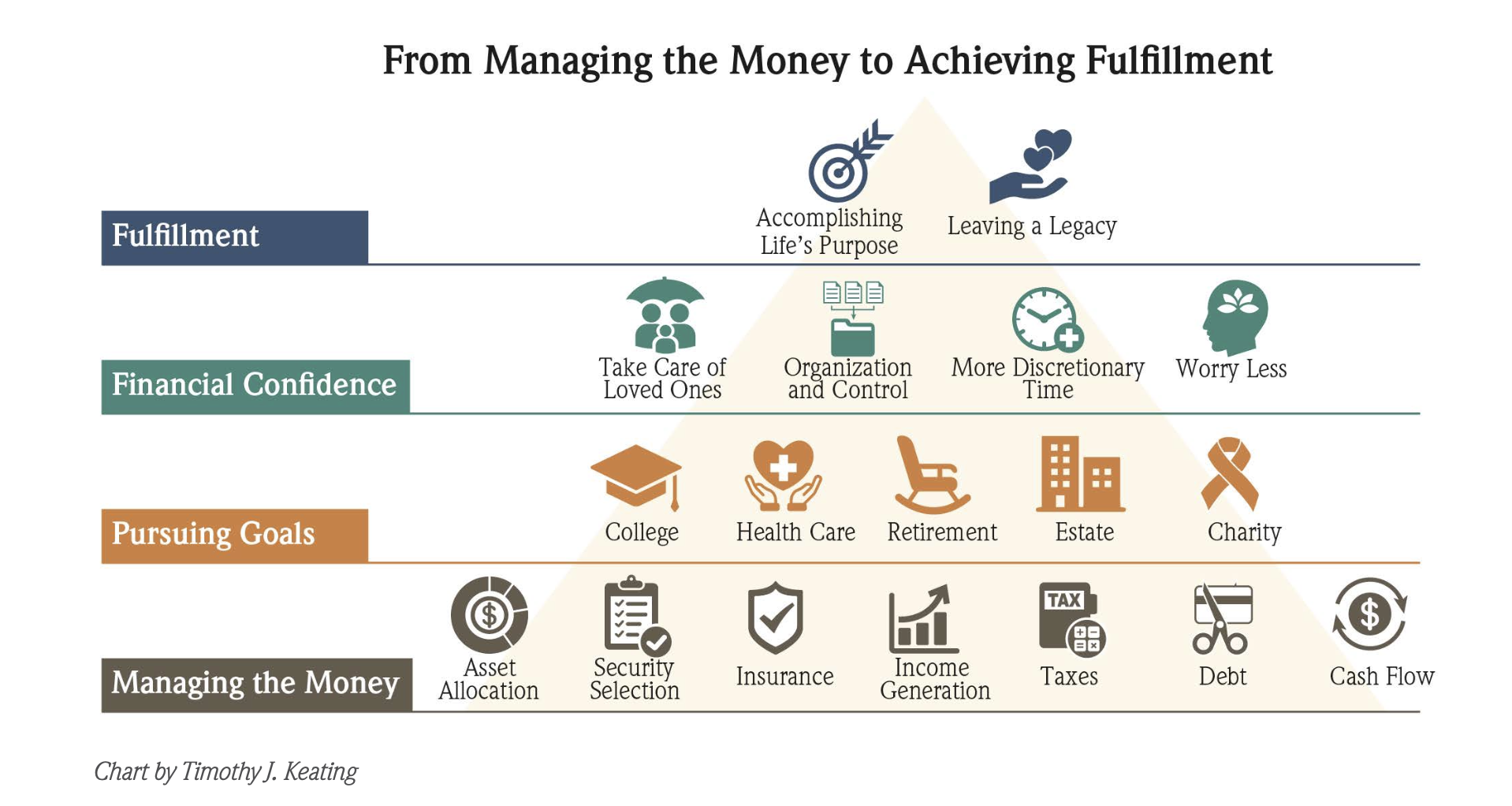

Start With Planning, Not Products

In the aftermath of divorce, most clients aren't asking, "How much should I allocate to private equity?" They’re asking, “How much do I need to live comfortably and maintain my lifestyle?”

Will I have enough?

What can I safely spend, gift, or give away?

What happens if I get sick or hospitalized, and what type of insurance do I need?

How much will I be able to leave to the kids?

These are planning questions—not investment questions. And the answers depend on a comprehensive understanding of the client's income, expenses, taxes, health care needs, insurance, estate goals, and long-term obligations.

Too often, advisory firms lead with portfolios and products, skipping over the life context that should drive every decision. The best advisors reverse this: they begin with the plan and then align the portfolio accordingly.

The portfolio is a tool and the medium to fund a financial plan—not the plan itself.

The following diagram illustrates this hierarchy of financial needs, starting at the bottom with managing the money and culminating in long-term fulfillment.

Raising the Bar: Ask for a One-Pager

One of the simplest, smartest ways to evaluate an adviser is to ask: "Can you show me—on one page—what I get as a client in exchange for the fees I will pay you?"

This request is an excellent filter. Advisers who can deliver a short, specific, plain-English summary are more likely to offer coherent, consistent advice. Those who can't are often compensating with volume.

Especially in divorce, clarity is a gift. Simplicity is a service.

Three Questions Every Out-Spouse Should Ask a Prospective Adviser

Family lawyers don't need to be financial experts. But they do need a framework for evaluating advisory candidates. These three questions reveal more than any marketing brochure:

How many high-net-worth divorce clients have you advised, and what's your approach in those situations?

What specific tools or platforms do you use to coordinate financial, tax, and legal planning across the client's advisory team?

How do you deliver value throughout the year—and how will my clients know what's been done on their behalf?

For attorneys and clients seeking a more comprehensive framework, see Appendix A: “10 Questions to Ask When Choosing a Wealth Adviser After a Divorce.”

Conclusion: Structure, Trust, and the Right Fit

There is no single correct answer when choosing a wealth adviser following a divorce. But there are good frameworks. Emotional trust must lead. Institutional reputation should follow—if at all.

Clients should seek a relationship where the adviser is accountable, the advice is transparent, and the planning is integrated. For family lawyers, asking the right questions is the first step toward securing that outcome.

In the end, it's not about brand. It's about fit. The most successful post-divorce transitions start with the right person in the trusted adviser seat. Family lawyers can play a pivotal role by helping clients ask the right questions to identify an adviser who fits their unique needs and circumstances.

Appendix A: 10 Questions to Ask When Choosing a Wealth Adviser After a Divorce

How many high-net-worth divorce clients have you advised, and what's your approach in those situations?

Will I be working directly with you, or will my relationship be handed off to junior team members or a service team?

What specific tools or platforms do you use to coordinate financial, tax, and legal planning across my advisory team?

How do you deliver value throughout the year, and how will I know what's been done on my behalf?

Can you share an anonymized example of how you helped simplify a complex post-divorce financial picture?

How do you help clients decide whether to keep, sell, or restructure major assets after a divorce?

How do you handle sensitive family dynamics, especially when adult children, former in-laws, or shared business interests are in the picture?

Do you have a written framework or narrative that explains how you determine the amount of capital required to support a lifetime of spending—and what can safely be spent, gifted, or repositioned?

How do you help clients estimate their true living expenses, especially when past spending may not reflect future reality?

Do you have a clear, plain-English explanation of how you build investment portfolios and how your approach aligns with long-term planning goals?

Appendix B: Jason Zweig's 19 Questions to Ask Your Financial Adviser

Jason Zweig is a widely respected financial columnist for The Wall Street Journal and one of the most authoritative voices on investor behavior and ethical advisory practices. While Appendix A focuses specifically on the unique needs of divorcing clients, Zweig's questions apply broadly to anyone seeking trustworthy, transparent advice.

Are you always a fiduciary, and will you state that in writing?

Does anybody else ever pay you to advise me and, if so, do you earn more to recommend certain products or services?

Do you participate in any sales contests or award programs creating incentives to favor particular vendors?

Will you itemize all your fees and expenses in writing?

Are your fees negotiable?

Will you consider charging by the hour or retainer instead of an annual fee based on my assets?

Can you tell me about your conflicts of interest, orally and in writing?

Do you earn fees as an adviser to a private fund or other investments that you may recommend to clients?

Do you pay referral fees to generate new clients?

Do you focus solely on investment management, or do you also advise on taxes, estates, retirement, budgeting and debt management, and insurance?

Do you earn fees for referring clients to specialists like estate attorneys or insurance agents?

What is your investment philosophy?

Do you believe in technical analysis or market timing?

Do you believe you can beat the market?

How often do you trade?

How do you report investment performance?

Which professional credentials do you have, and what are their requirements?

After inflation, taxes, and fees, what is a reasonable estimated return on my portfolio over the long term?

Who manages your money?

About the Authors

Jennifer Crum, AAML

Hanson Family Law Group

Jennifer Crum is a Certified Family Law Specialist and Partner at Hanson Family Law Group, with nearly 30 years of experience guiding Silicon Valley's high-net-worth clients. She specializes in cases involving venture capital, hedge funds, private equity, privately held companies, and real estate interests. A UC Berkeley and USF Law alumna, Jennifer is a Fellow of the American Academy of Matrimonial Lawyers. She can be reached at JC@hansonflg.com.

Timothy J. Keating

Cerity Partners

Timothy J. Keating is a partner and wealth adviser at Cerity Partners. He provides planning-first financial advice to individuals navigating major life transitions, including divorce, and specializes in post-divorce investment strategy, tax coordination, and estate planning. Mr. Keating is the author of numerous white papers on capital markets topics ranging from IPOs to the Yale Endowment model of investing. He held senior management positions at Bear Stearns, Nomura, and Kidder, Peabody in London and New York, and is a 1985 graduate of Harvard College. He can be reached at TKeating@ceritypartners.com.